13-Week Cash Forecasting for Staffing Firms

Most staffing owners understand profit. What they can’t tolerate is cash uncertainty.

Payroll hits every week or two. Client payments show up when they feel like it. And the moment you are a little off, the bank balance starts doing things you did not expect.

A 13-week cash forecast fixes that. It turns cash from a mystery into a managed system.

This post showcases a simple framework and a weekly process to build and run a rolling cash forecast so cash surprises stop.

Why 13 weeks is the sweet spot

You can forecast a year, but it will not stay accurate. You can forecast a week, but it will not give you enough warning.

Thirteen weeks is the middle ground. It is long enough to see problems coming, and short enough to be updated weekly without turning into a finance project.

For staffing firms, it also matches the reality of AR timing. Most of your cash problems are not twelve months away. They are 2 to 8 weeks away.

What a cash forecast is, in plain English

A cash forecast is a week-by-week view of:

cash coming in (collections, not revenue)

cash going out (payroll first, then everything else)

ending cash balance

It is not budgeting. It is not accounting. It is a tool to answer one question:

Will we have enough cash to cover payroll and stay in control?

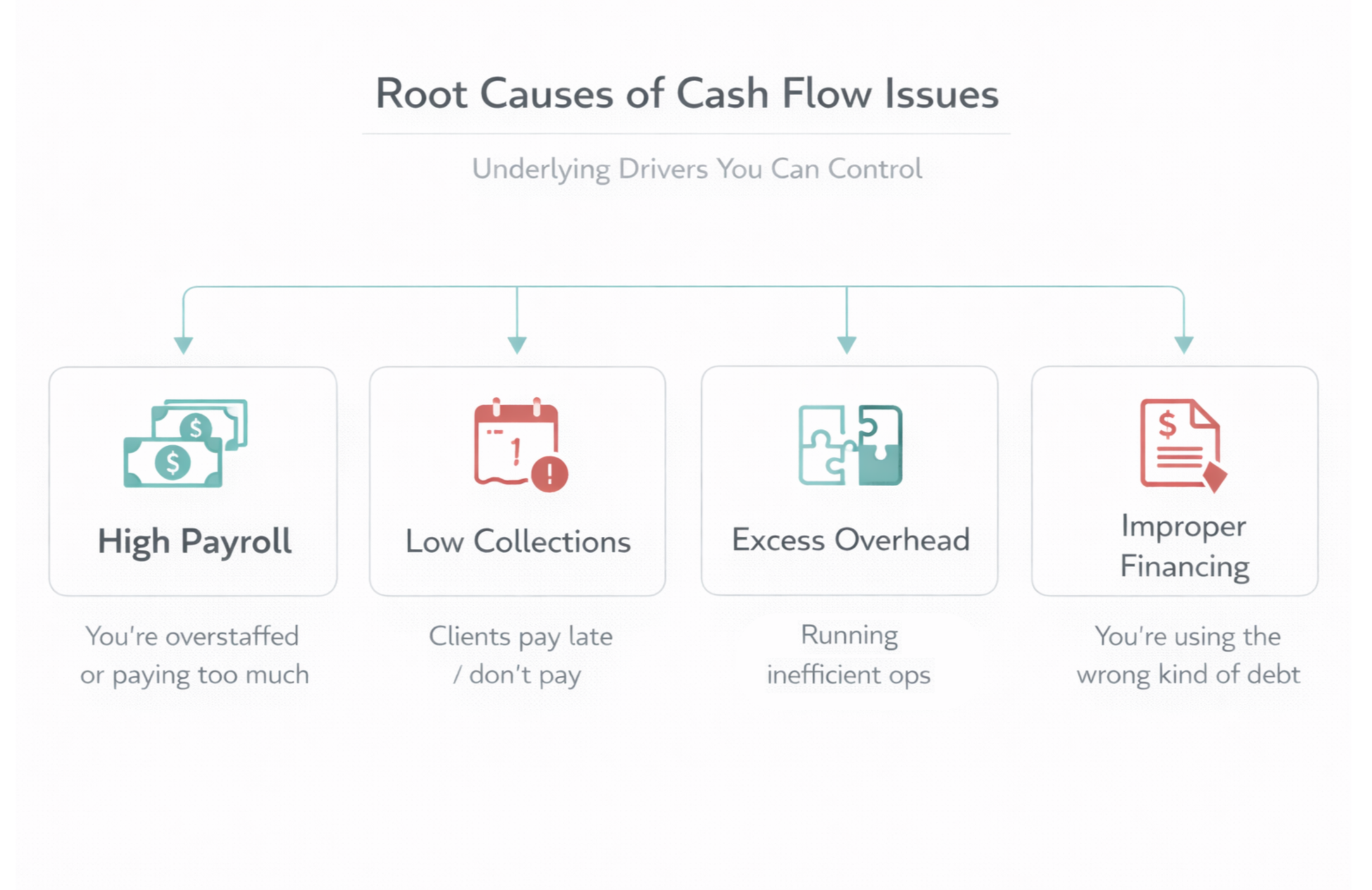

Staffing inputs you need (and what most firms forget)

A staffing cash forecast is not complicated, but it must reflect staffing reality. Your key inputs are:

Cash in (collections):

expected client payments by week

realistic timing assumptions (not what you wish would happen)

Cash out (payments):

payroll schedule (weekly/biweekly)

employer payroll taxes tied to payroll

workers’ comp timing and any true-ups

benefits tied to temp labor (if applicable)

operating expenses that hit cash (rent, software, insurance, marketing)

debt payments, LOC interest, factoring fees (if you use them)

owner draws (yes, include them)

Most forecasts fail because owners track revenue, not collections, and they understate payroll burden. In staffing, that is a fast way to get blindsided.

The simplest 13-week template

You can build this in Excel or Google Sheets. Keep it simple.

Each row is a week. Each column is a category.

For each week:

Beginning cash

Plus: expected collections

Minus: payroll (wages)

Minus: payroll burden (taxes, workers’ comp, benefits)

Minus: operating expenses

Minus: debt/financing payments

Equals: ending cash

Then the next week begins with the prior week’s ending cash.

That is the entire engine.

If you want a little more detail, break operating expenses into fixed and variable. Do not overbuild it. The power comes from updating it weekly, not from perfect categories.

The two drivers that matter most

There are only two numbers that really move the forecast:

Driver 1: What you will collect (not what you billed)

Collections are the hard part because they require judgment.

A simple approach that works:

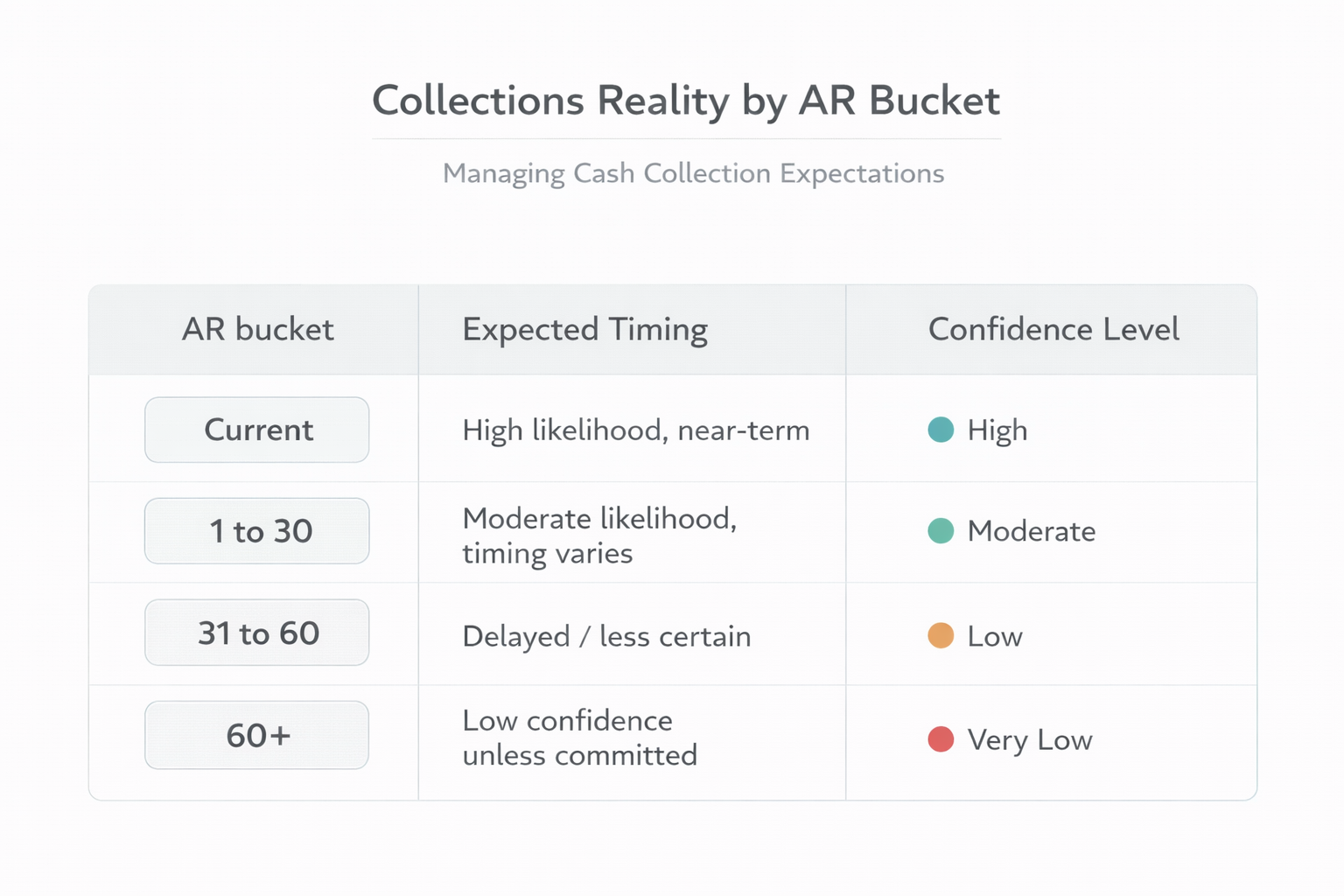

Start with your AR aging report.

Group it into buckets: Current, 1–30, 31–60, 60+.

Apply conservative collection expectations to each bucket.

For example:

Current: most will pay soon, but not all this week

1–30: likely, but timing varies

31–60: assume delays and disputes

60+: assume slow collection unless you have a known commitment

Then layer in known items:

“Client A pays every other Friday.”

“That large invoice is under dispute.”

“Client B always pays on the 15th.”

The goal is not to be perfect. The goal is to be honest.

Driver 2: What you must pay (payroll first)

Payroll is your heartbeat. Put payroll in first, then add the burden.

Staffing firms often forget to include:

employer payroll taxes

workers’ comp cash timing

payroll processing fees

benefits tied to temp labor

If payroll is $200k, plan for more than $200k leaving the account.

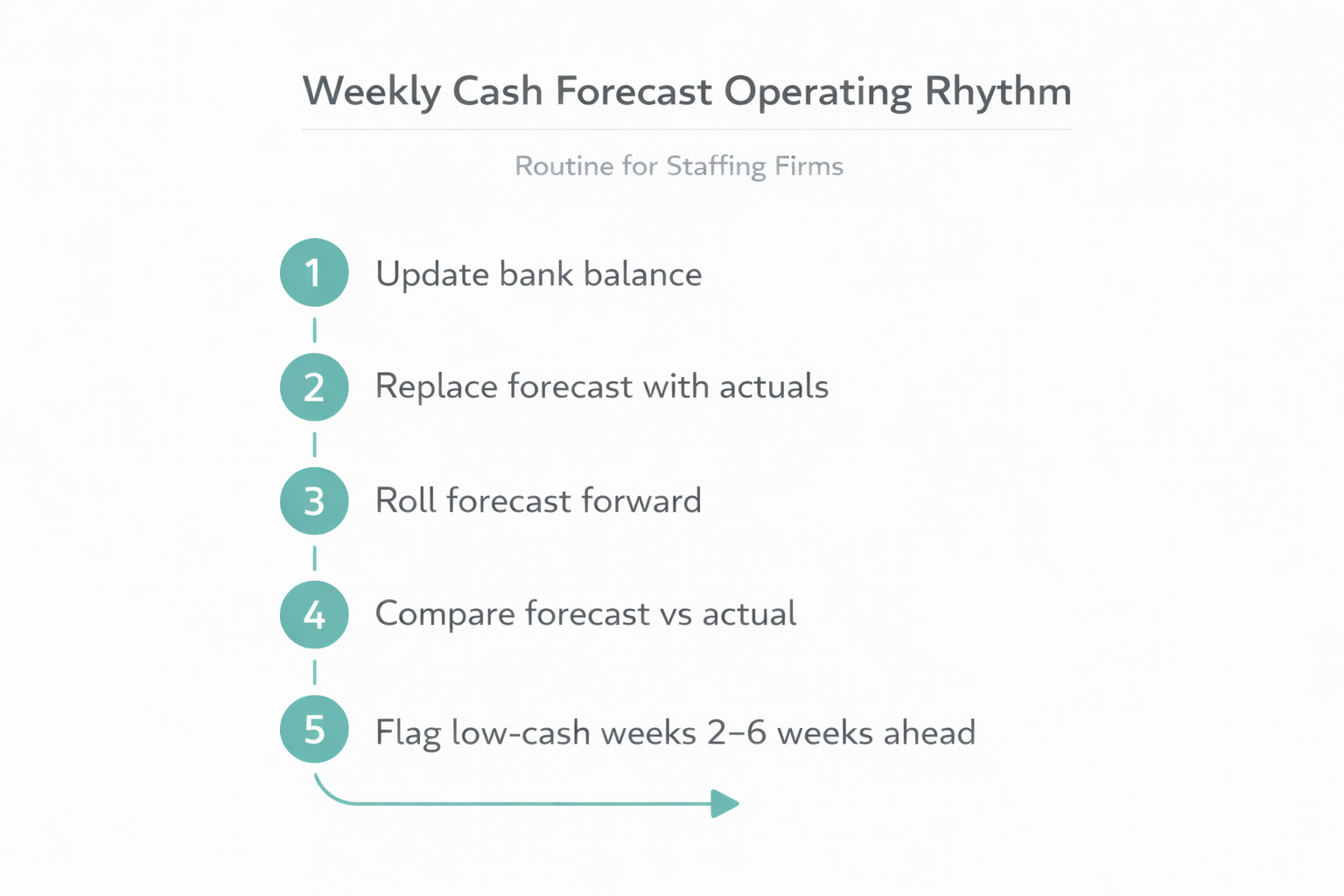

The weekly process that makes this work

A cash forecast is only valuable if it becomes an operating ritual.

Here is a simple rhythm:

Every Monday (or right after payroll runs):

Update beginning cash to match your bank balance.

Replace last week’s forecast with actual collections and actual payments.

Roll the forecast forward one week (always keep 13 weeks visible).

Compare forecast vs actual and write down why the variance happened.

Look ahead 2–6 weeks: identify the low-cash week before it arrives.

That last step is the whole point. You want to see the dip coming early enough to do something about it.

What actions the forecast enables

Once you can see cash pressure coming, you get options:

tighten timecard approvals and send invoices faster

run a real weekly collections cadence

adjust hiring timing

slow growth temporarily if working capital is strained

pull from a LOC earlier, when you still have leverage

reduce owner draws during a predictable dip

renegotiate terms with chronic slow payers

Without a forecast, you react when you are already in the problem. With a forecast, you act while you still have choices.

Common mistakes to avoid

Confusing revenue with collections

Being overly optimistic about AR timing

Ignoring payroll burden and true-up timing

Forgetting debt service, factoring fees, or quarterly expenses

Building it once and not updating weekly

If you are not updating it weekly, it is just a spreadsheet. Update it weekly, and it becomes a tool you can run the business from.

Final Thought

A stable cash position is not about guessing. It’s about visibility into what you will collect and what you must pay.

If cash surprises keep happening, it usually means you do not have a consistent forecast and a weekly cadence to keep it accurate.

In our free Accounting Review, we help staffing firm owners build a simple 13-week forecast and tighten the inputs behind it, so you can see cash pressure early and stay in control.