A Staffing Firm Chart of Accounts That Makes Your Numbers Decision-Ready

Your chart of accounts does more than organize transactions.

It determines whether your financial reports are useful or confusing.

Many staffing and recruiting firms technically have books. They have a profit and loss statement. They have a balance sheet. They may even have monthly financials.

But the real question is:

Do those reports help you make better decisions?

For many staffing firm owners, the answer is no.

The problem is not always bad bookkeeping. Often, the problem is that the chart of accounts was set up like a generic small business, not like a staffing firm.

This article explains what a staffing firm chart of accounts should help you see, where generic accounting structures fall short, and how to organize your numbers so they become decision-ready.

What a Chart of Accounts Is

A chart of accounts is the structure behind your financial reports.

It tells your accounting system how to categorize:

Revenue

Direct costs

Payroll costs

Operating expenses

Assets

Liabilities

Equity

At a basic level, it is the foundation of your financial reporting.

But in a staffing firm, the chart of accounts should do more than produce a clean tax return.

It should help answer questions like:

Which revenue streams are most profitable?

Are contractor margins holding up?

How much does delivery actually cost?

Are payroll taxes and workers’ comp being captured correctly?

Are internal recruiting costs being mixed with direct labor?

Which parts of the business are scaling profitably?

A generic chart of accounts usually cannot answer those questions clearly.

Why Generic Charts of Accounts Fail Staffing Firms

Many staffing firms start with a basic accounting setup.

Revenue goes into one income account.

Payroll goes into one payroll account.

Software, insurance, commissions, recruiting costs, and administrative costs are grouped wherever they seem to fit.

That may be fine when the firm is small.

But as the business grows, the reports become less useful.

The owner may see total revenue, total payroll, and total profit, but not the details that actually matter.

For staffing firms, the difference between useful and useless financials often comes down to whether the chart of accounts separates the right categories.

A staffing firm needs visibility into margin, delivery cost, payroll burden, recruiter costs, client profitability, and overhead.

Without that structure, financial reports become summaries instead of decision-making tools.

The Core Problem: Revenue and Costs Get Blended Together

The biggest issue in many staffing firm financials is blending.

Temporary staffing revenue gets mixed with permanent placement revenue.

Contractor wages get mixed with internal wages.

Payroll taxes get buried in general payroll expense.

Workers’ comp gets treated like a general insurance cost.

Recruiter commissions get grouped with general payroll.

Software gets buried in miscellaneous.

When everything is blended together, the owner may still have financial statements that look clean.

But clean does not mean useful.

The numbers may be accurate in total while still hiding the information needed to run the firm.

What a Decision-Ready Chart of Accounts Should Show

A decision-ready chart of accounts should make your financial reports easier to interpret.

It should help separate the major parts of the business so you can see what is really happening.

At a minimum, staffing firms should be able to see:

Revenue by service line

Direct labor costs

Payroll taxes and burden

Workers’ comp costs

Gross margin by major revenue type

Internal payroll and overhead

Recruiter or sales compensation

Software and operating tools

Client-related costs

General administrative expenses

The goal is not to create hundreds of accounts.

The goal is to create enough structure so the reports tell the right story.

Revenue Should Be Separated by Business Model

Revenue is not all the same.

A staffing firm may have several types of revenue, including:

Temporary staffing revenue

Contract staffing revenue

Direct hire or permanent placement revenue

Retained search revenue

Temp-to-perm conversion fees

Recruiting project fees

Other client service fees

These revenue streams behave differently.

Temporary staffing revenue usually comes with direct payroll costs, payroll taxes, and workers’ comp exposure.

Permanent placement revenue may have higher gross margin, but more volatility.

Retained search revenue may have different timing and collection patterns.

If all revenue is grouped together, the firm cannot clearly see which business model is driving profit and which one is consuming cash.

A good chart of accounts should separate revenue in a way that matches how the business is actually managed.

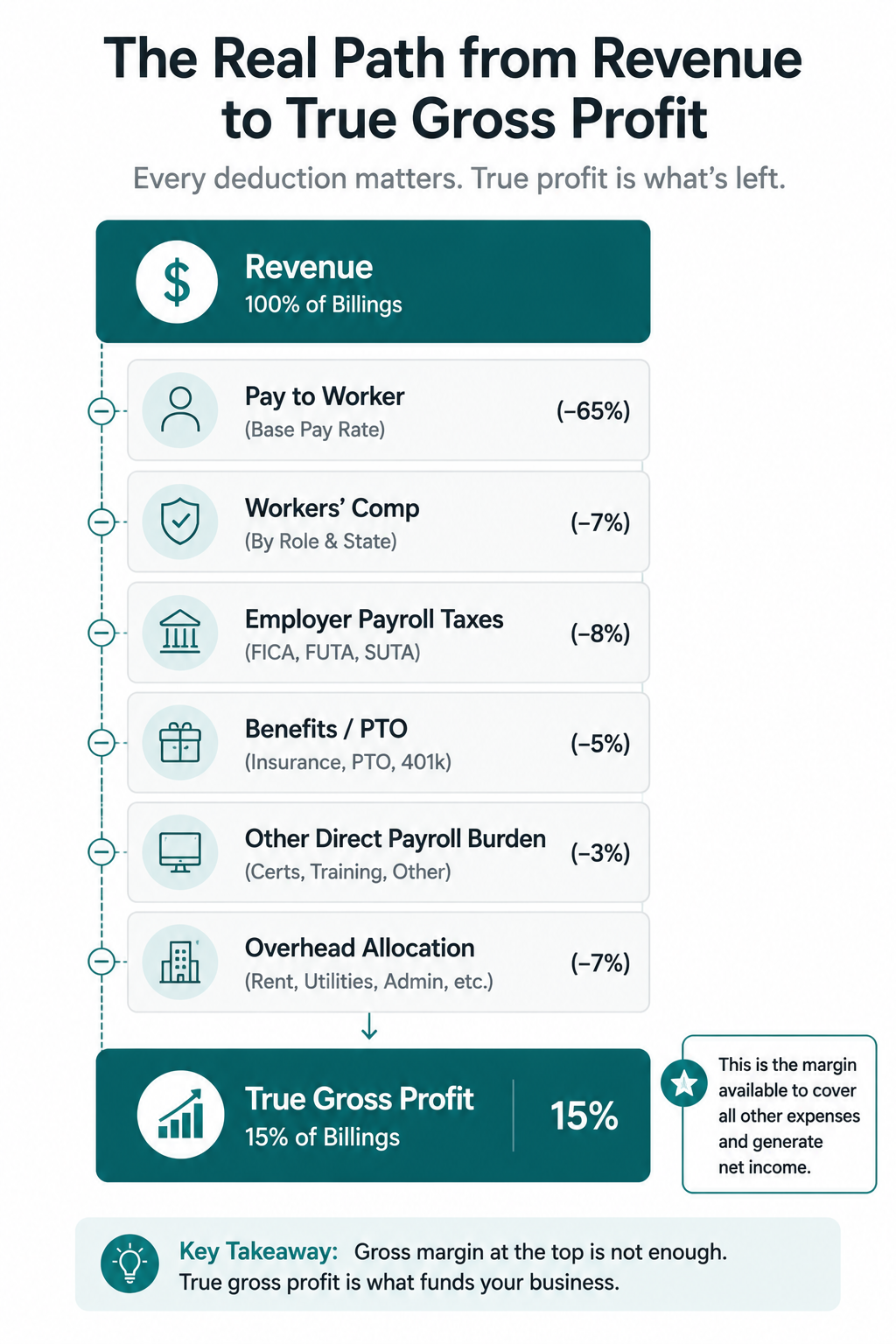

Direct Costs Should Match the Revenue They Support

Direct costs are the costs tied directly to delivering revenue.

For staffing firms, these often include:

Wages paid to placed employees

Employer payroll taxes

Workers’ comp

Benefits tied to placed employees

Background checks or screening costs

Drug testing

Credentialing or compliance costs

Job-specific payroll processing costs

These costs should usually sit above gross profit.

That allows the firm to calculate gross margin in a way that reflects the true cost of delivery.

One common mistake is treating some direct delivery costs as general overhead.

For example, workers’ comp may be posted to a general insurance account. Background checks may be buried in office expense. Payroll processing fees may be mixed with administrative software.

That makes gross margin look better than it really is.

The business may appear healthy at the gross margin level while delivery costs are quietly leaking into overhead.

Internal Payroll Should Not Be Mixed With Field Payroll

Staffing firms need a clear separation between field payroll and internal payroll.

Field payroll is the pay for workers placed with clients.

Internal payroll is the pay for the firm’s own employees, such as:

Recruiters

Salespeople

Account managers

Operations staff

Administrative staff

Finance or accounting staff

Owners on payroll

These are very different costs.

Field payroll is usually a direct cost tied to revenue.

Internal payroll is usually operating overhead.

When the two are mixed, gross margin becomes unreliable.

The firm may not know whether margin pressure is coming from client pricing, pay rates, recruiter compensation, or internal headcount.

That makes it harder to decide whether to raise rates, adjust pay, hire, cut costs, or improve productivity.

Payroll Burden Needs Its Own Visibility

Payroll burden is one of the most important areas in staffing firm accounting.

It can include:

Employer payroll taxes

Workers’ comp

State unemployment insurance

Benefits

Paid time off

Other employer-paid labor costs

If burden is not tracked clearly, pricing decisions become risky.

A firm may think it has enough spread between bill rate and pay rate, but the true burden may be higher than expected.

This is especially important for temporary staffing firms, healthcare staffing firms, industrial staffing firms, and any firm with high payroll volume.

A decision-ready chart of accounts should make payroll burden visible enough to support pricing and margin analysis.

The owner should not have to guess whether the spread is enough.

Gross Margin Should Be Easy to Read

Gross margin is one of the most important numbers in a staffing firm.

But it is only useful if the chart of accounts supports it.

A good gross margin section should make it easy to see:

Total revenue

Direct labor costs

Employer taxes and burden

Workers’ comp

Other direct delivery costs

Gross profit

Gross margin percentage

For firms with multiple service lines, gross margin should ideally be visible by business model.

For example:

Temporary staffing gross margin

Contract staffing gross margin

Permanent placement gross margin

Recruiting project gross margin

This helps prevent one strong revenue stream from hiding weakness in another.

A staffing firm can have a good overall gross margin while one segment is underpriced, overburdened, or cash-intensive.

Operating Expenses Should Be Useful, Not Overcomplicated

The operating expense section should be clean and practical.

Common staffing firm operating expense categories include:

Internal salaries and wages

Recruiter commissions

Sales commissions

Payroll processing fees

Recruiting software

Job boards

Applicant tracking system

CRM software

Professional services

Marketing

Insurance

Rent or office costs

Travel and meals

Training and education

General administrative software

Bank and financing fees

The key is to avoid both extremes.

Too few accounts create vague reports.

Too many accounts create clutter.

For example, “Software” may be too broad if the firm uses many important tools. But creating a separate account for every small subscription may be unnecessary.

A useful structure might separate:

Recruiting software

Job boards

CRM and sales tools

Accounting and admin software

General subscriptions

That gives the owner better visibility without overwhelming the report.

The Balance Sheet Matters Too

A staffing firm chart of accounts is not just about the profit and loss statement.

The balance sheet matters because staffing firms often deal with timing gaps.

Important balance sheet accounts may include:

Accounts receivable

Payroll liabilities

Payroll tax liabilities

Workers’ comp payable

Accrued wages

Line of credit balance

Credit card balances

Owner distributions

Sales tax or other state liabilities, if applicable

Accounts receivable is especially important.

A staffing firm can look profitable on the income statement while cash is tied up in unpaid invoices.

The chart of accounts should support clean tracking of receivables, payroll liabilities, and debt.

This helps the owner understand whether cash pressure is coming from operations, collections, growth, or financing.

Warning Signs Your Chart of Accounts Is Not Working

A weak chart of accounts usually shows up indirectly.

Common warning signs include:

Gross margin changes every month without a clear reason

Payroll costs are hard to separate by type

Workers’ comp is buried in general insurance

Revenue streams are all grouped together

Internal payroll and contractor payroll are mixed

Too many expenses are posted to miscellaneous

The owner needs spreadsheets to understand basic margins

Financial reports are accurate but not helpful

Cash flow feels tight even when profit looks fine

If these feel familiar, the issue may not be the accounting software.

It may be the structure underneath the reports.

What to Fix Before Adding Dashboards

Many firms want dashboards.

Dashboards can be useful, but only if the underlying numbers are organized correctly.

A dashboard built on a messy chart of accounts will just make messy numbers look more polished.

Before building dashboards, staffing firm owners should make sure the accounting system can clearly separate:

Revenue types

Direct labor

Payroll burden

Workers’ comp

Internal payroll

Recruiter and sales costs

Operating overhead

Receivables and payroll liabilities

The accounting structure comes first.

The dashboard comes second.

A Simple Staffing Firm Chart of Accounts Framework

A practical staffing firm chart of accounts might follow this structure:

Revenue

Temporary staffing revenue

Contract staffing revenue

Permanent placement revenue

Conversion fees

Other service revenue

Direct costs

Field employee wages

Employer payroll taxes

Workers’ comp

Benefits for placed employees

Screening and compliance costs

Other direct delivery costs

Gross profit

Revenue minus direct costs

Operating expenses

Internal salaries and wages

Recruiter commissions

Sales commissions

Recruiting tools and job boards

Software and subscriptions

Marketing

Professional services

Insurance

Office and administrative costs

Travel and meals

Training

Bank fees and financing costs

Balance sheet

Cash

Accounts receivable

Payroll liabilities

Workers’ comp payable

Line of credit

Credit cards

Owner equity and distributions

This does not need to be the exact structure for every firm.

The right chart of accounts depends on the firm’s business model, service mix, and reporting needs.

But the principle is the same:

Your chart of accounts should reflect how the business actually makes money.

Final Thought

A staffing firm chart of accounts should not just help you file taxes.

It should help you run the business.

When revenue, payroll, burden, workers’ comp, internal costs, and overhead are organized clearly, your financials become more than reports.

They become decision tools.

If your numbers are technically accurate but still hard to use, the chart of accounts may be the first place to look.

In our Accounting Review, we help staffing firm owners evaluate whether their chart of accounts is giving them the visibility they need to understand margins, cash flow, and profitability with confidence.