Misclassified Costs That Inflate Staffing Gross Margin (And Hide the Real Problem)

If your staffing firm’s gross margin looks strong on paper but cash is tight, payroll feels stressful, or profit does not match the effort, there’s a good chance your gross margin is inflated.

The most common cause is not pricing. It’s misclassified costs.

When the wrong expenses land in the wrong accounts, your gross margin becomes unreliable. That makes benchmarks useless and leads you to “fix” the wrong problem.

Why cost classification matters for staffing firm gross margin

In staffing and recruiting, gross margin is an operating metric. Owners use it to decide:

Are we pricing correctly?

Which service lines are actually profitable (temp, perm, direct hire)?

Can we afford to hire another recruiter?

Which clients are quietly hurting the business?

Those decisions only work if your P&L is structured correctly and costs are classified consistently. If not, your “gross margin” becomes a vanity number and the real issue shows up later as cash stress.

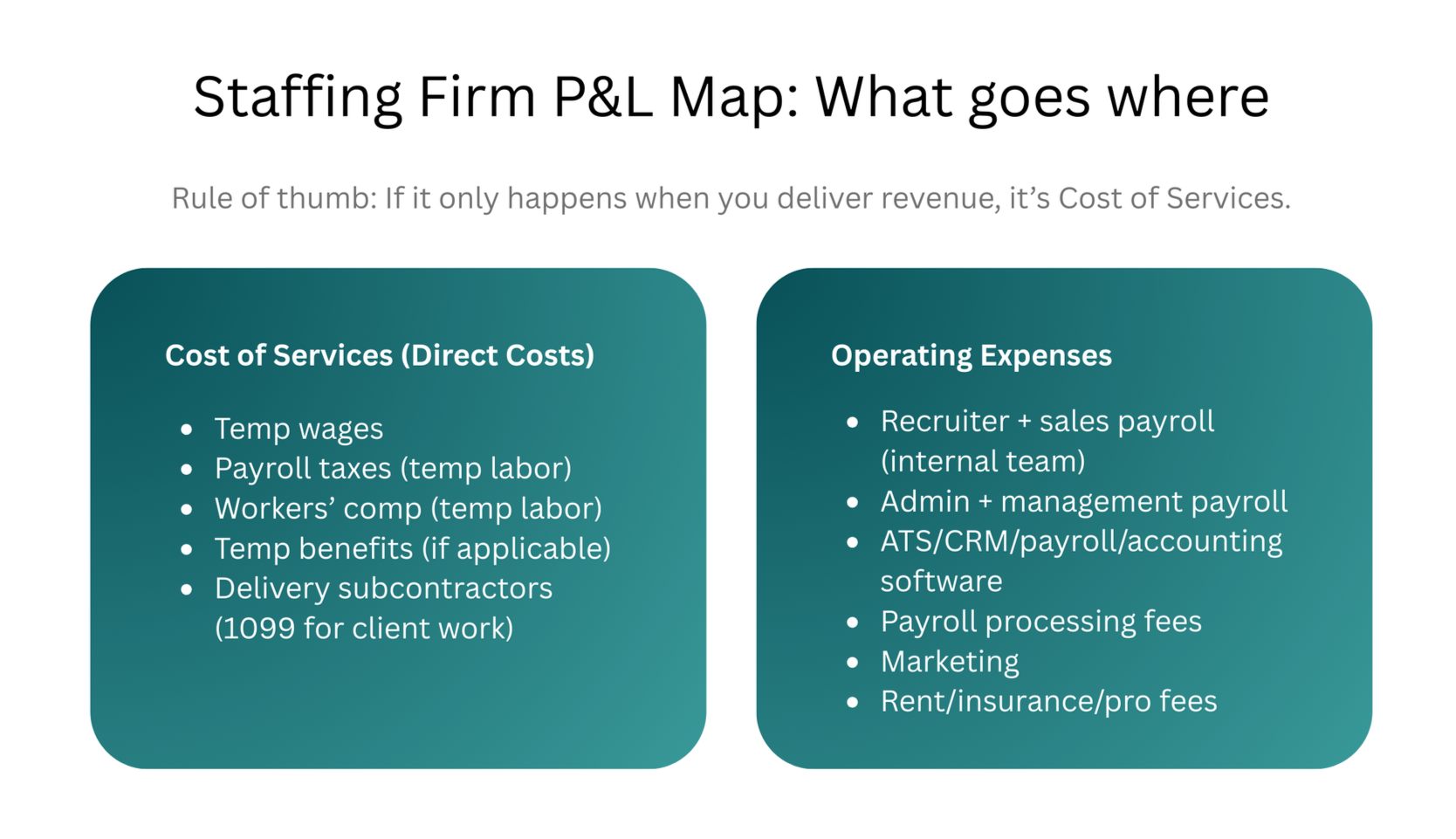

What belongs in staffing firm COGS vs operating expenses

Cost of Services (COGS) should include direct delivery costs, typically:

Temp payroll (wages paid to assigned employees)

Employer payroll taxes on temp payroll

Workers’ comp tied to temp payroll

Benefits tied to temp payroll (if applicable)

Subcontractor/1099 costs when they fulfill client work

Operating expenses (Opex) should include overhead and growth costs, typically:

Recruiter and sales payroll (internal staff)

Admin and management payroll

Software (ATS, CRM, payroll, accounting tools)

Payroll processing/platform fees

Rent, insurance, professional fees, marketing

Now here’s where things commonly go wrong.

The most common misclassified costs that inflate staffing gross margin

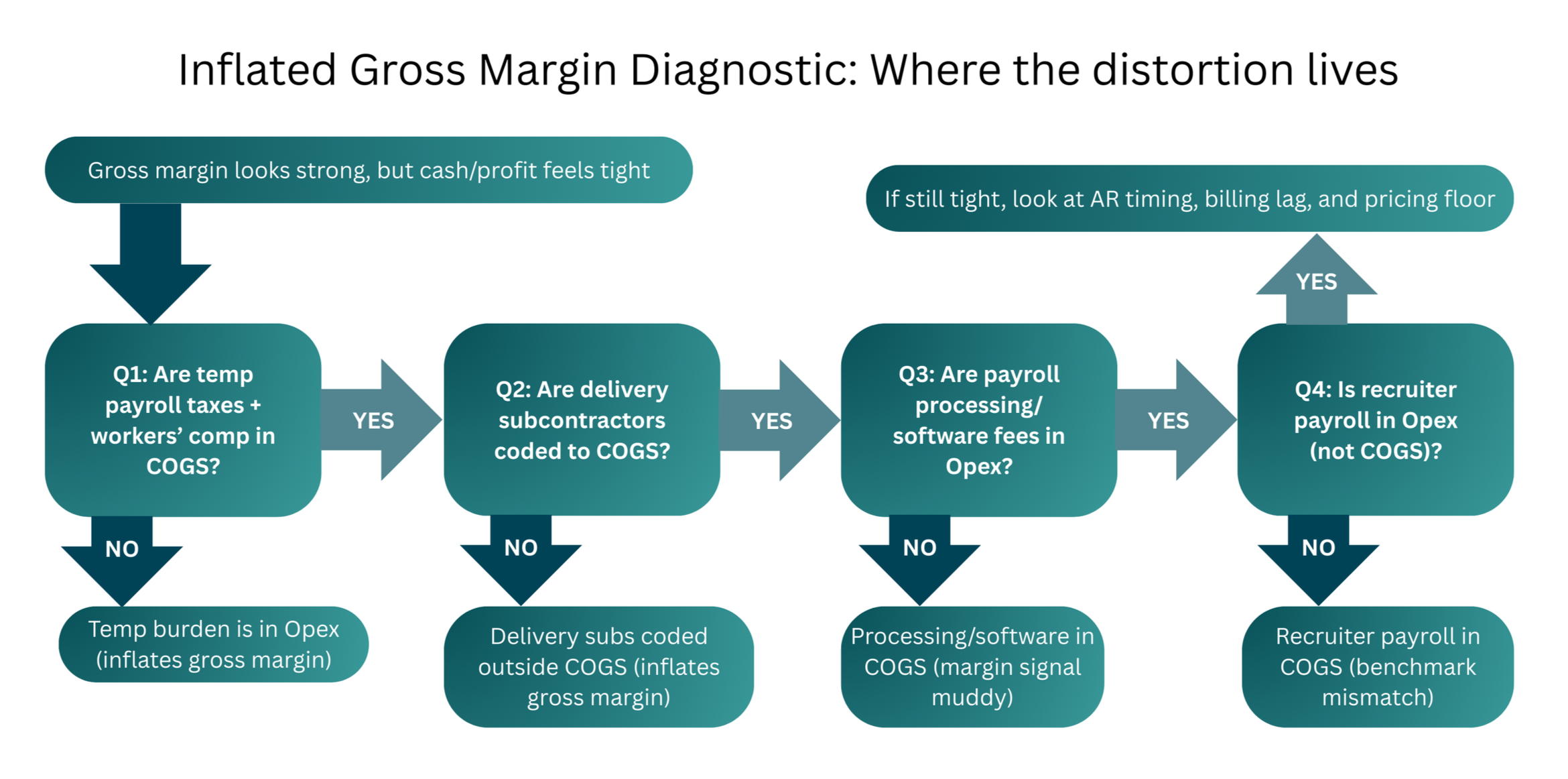

1) Temp payroll taxes and workers’ comp recorded in operating expenses

If you run temp staffing, payroll burden costs are part of delivering the service. They belong in COGS.

What happens when they’re in Opex: gross margin looks higher than it really is, pricing feels fine on paper, and the “true margin” shows up later as weak operating profit.

Fix: create dedicated COGS accounts like:

Payroll Taxes – Temp Labor

Workers’ Comp – Temp Labor

Then ensure your payroll system or monthly journal entries map them correctly.

2) Subcontractor/1099 delivery costs coded outside COGS

If a contractor is directly fulfilling billable client work, that cost is Cost of Services. Too often, it gets coded as “Contract Labor” under operating expenses or “Professional Fees.”

What happens: gross margin is inflated and client profitability analysis becomes unreliable.

Fix: use a rule: if the contractor fulfills client work tied to revenue delivery, it’s COGS. If they support internal operations (marketing contractor, admin help), it’s Opex. Document it and enforce it.

3) Payroll processing fees buried in COGS

Payroll processing and platform fees feel “related to payroll,” so firms often dump them into COGS. But these fees are overhead, not direct delivery costs.

What happens: it muddies the margin signal and makes comparisons to benchmarks harder.

Fix: move payroll processing/platform fees into Opex under accounts like Payroll Processing Fees or Software Subscriptions.

4) Recruiter payroll classified as COGS

Recruiter and sales payroll generally belongs in operating expenses. It supports revenue generation, not the direct delivery cost of each dollar of revenue.

What happens: gross margin becomes distorted and stops matching staffing industry benchmarks.

Fix: keep recruiter payroll in Opex, and track productivity with KPIs instead (gross profit per recruiter, spread per hour, placements per month).

How to tell if your gross margin is inflated

A few warning signs:

Gross margin looks “too good,” but cash flow stays tight

Margin is stable while operating profit swings wildly

Payroll reports do not tie cleanly to COGS

You have large “miscellaneous” or “uncategorized” balances each month

If any of these are true, you likely have classification leakage.

A simple fix process (no full rebuild required)

Pull a trailing 12-month P&L and payroll summary.

Identify gross-margin-related costs (temp payroll burden, workers’ comp, delivery subcontractors).

Write a one-sentence rule for each gray area (what is COGS vs Opex).

Reclass the last 3–6 months first so decisions improve immediately.

Lock the workflow by updating payroll mappings, bank rules, and recurring entries.

Final Thought

A healthy gross margin is not just about pricing. It’s about clean reporting that tells you the truth.

If your gross margin looks strong but the business still feels tight, your costs may be misclassified and your margin may be inflated.

In our free Accounting Review, we review your P&L structure and break down delivery costs so you can see what your true gross margin is and what needs to be fixed.