Workers’ Comp and Burden Rates: The Right Way to Model True Delivery Cost

As you run your firm, you probably know your pay rates and bill rates.

But do you know your true delivery cost?

Many staffing firm owners look at the spread between what they bill the client and what they pay the worker. That is a useful starting point, but it is not the full picture.

In staffing, the real cost of delivering labor includes more than wages. Payroll taxes, workers’ comp, benefits, insurance, compliance, and other burden costs can quietly eat into margin.

This article explains how workers’ comp and burden rates affect true delivery cost, why averages can be misleading, and how to model staffing profitability more accurately.

What Delivery Cost Means in a Staffing Firm

At a basic level, delivery cost means:

The total cost required to place and pay a worker for a client

For staffing firms, this usually includes:

Worker wages

Employer payroll taxes

Workers’ compensation insurance

Benefits tied to the worker

State unemployment insurance

Federal unemployment insurance

Other payroll-related burden costs

Delivery cost does not usually include:

Internal recruiter salaries

Sales commissions

Office rent

Software

General admin overhead

Owner compensation

Those costs still matter, but they are usually below gross margin.

Delivery cost answers one important question:

How much does this placement actually cost us before overhead and profit?

If that number is wrong, your margin calculation is wrong too.

Why Pay Rate Alone Is Not Enough

Many staffing firms think about profitability using a simple spread:

Bill rate minus pay rate

For example:

Bill rate: $40/hour

Pay rate: $28/hour

Spread: $12/hour

At first glance, that might look healthy.

But the firm does not keep the full $12.

Out of that spread, the firm still needs to cover payroll taxes, workers’ comp, benefits, insurance burden, admin costs, and profit.

If the true burden on that worker is $5/hour, the real gross profit is not $12/hour.

It is closer to $7/hour before overhead.

That difference matters.

A placement can look profitable on the surface while barely contributing to the business.

What Burden Rate Means

Burden rate is the extra cost of employing a worker beyond their base wage.

In staffing, burden usually includes:

Employer payroll taxes

Workers’ compensation insurance

Unemployment taxes

Benefits

Paid time off, if applicable

Payroll processing costs

Other required employer costs

A simple way to think about it is:

Pay rate + burden = true labor cost

If a worker is paid $28/hour and the burden rate is 18%, the true labor cost is:

$28.00 + $5.04 = $33.04/hour

If the client is billed $40/hour, the actual gross margin is based on $40 minus $33.04, not $40 minus $28.

That means the real gross profit is $6.96/hour.

Not $12/hour.

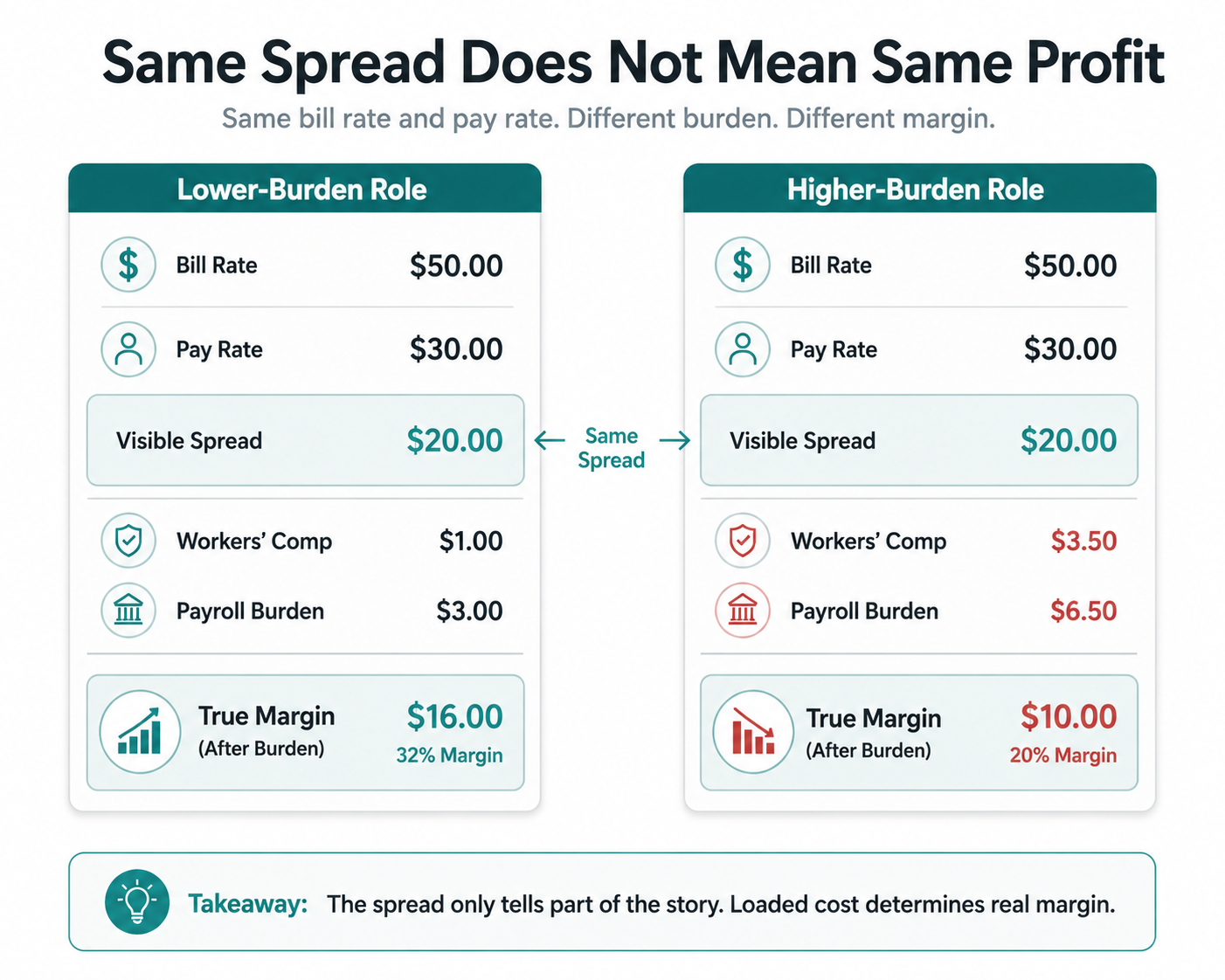

Why Workers’ Comp Deserves Special Attention

Workers’ comp is one of the most important burden costs in staffing because it can vary dramatically by role.

A clerical placement and a warehouse placement may have similar pay rates, but very different workers’ comp costs.

That means two placements with the same bill rate and pay rate can produce very different margins.

For example:

Administrative role

Pay rate: $25/hour

Bill rate: $35/hour

Lower workers’ comp cost

Light industrial role

Pay rate: $25/hour

Bill rate: $35/hour

Higher workers’ comp cost

On paper, the spread looks identical.

In reality, the second placement may be far less profitable because the risk and insurance burden are higher.

This is why modeling workers’ comp as one average percentage can be dangerous.

The Problem With Average Burden Rates

Average burden rates are easy to use, but they can hide real profitability problems.

A firm might use one standard burden rate across all placements, such as 15% or 18%.

That may work for rough estimates, but it can distort margin by:

Understating high-risk roles

Overstating low-risk roles

Making some clients look more profitable than they are

Hiding pricing problems by job type

Creating false confidence in blended gross margin

The issue is not that averages are useless.

The issue is that averages are not precise enough for decision-making.

If your firm serves multiple industries, job types, or risk categories, one burden rate is probably too simple.

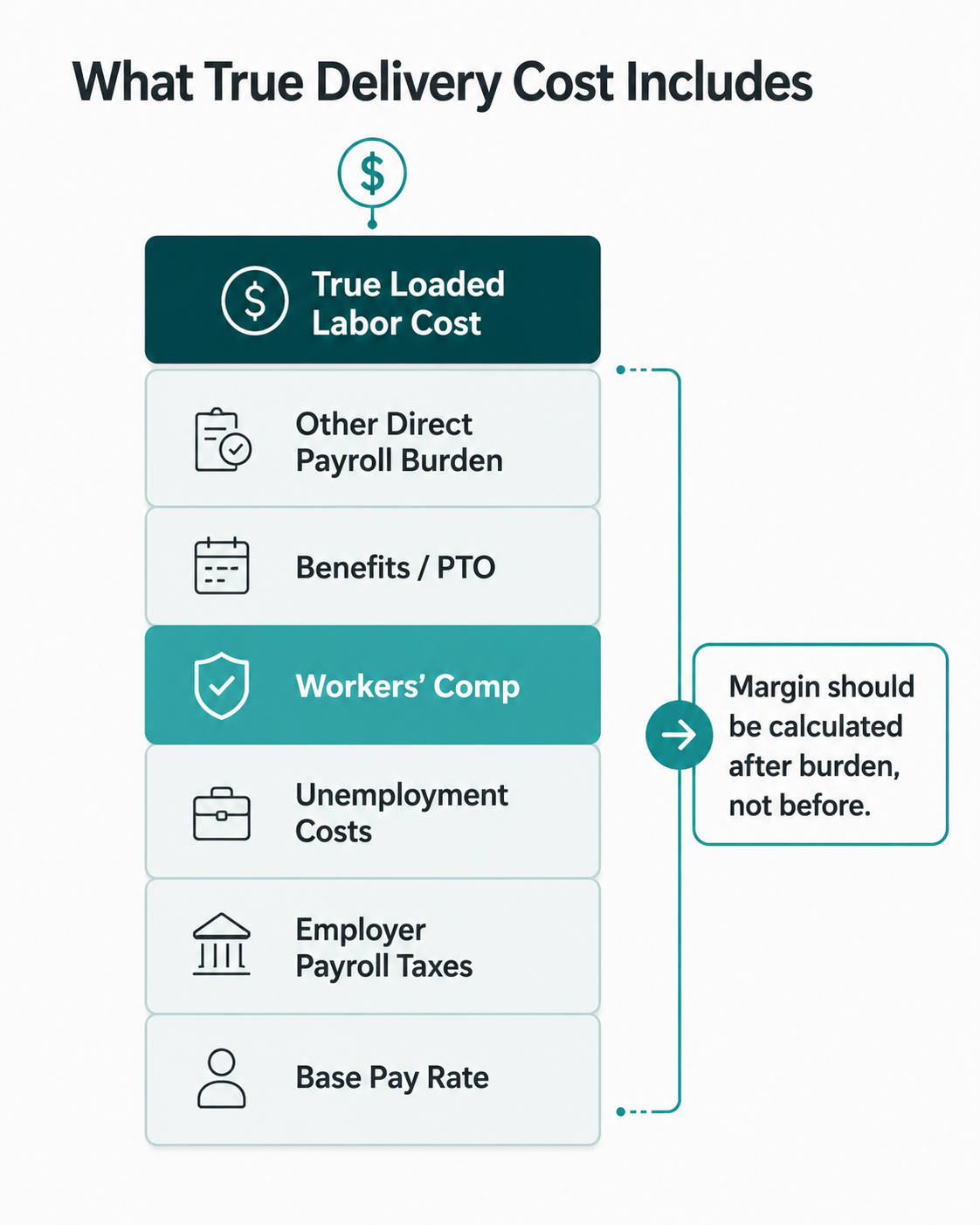

The Right Way to Model True Delivery Cost

A better model separates the major components of delivery cost.

Instead of using only pay rate, staffing firms should model:

Base wage

Employer payroll taxes

Workers’ comp by class or role

Benefits by worker type

Unemployment cost assumptions

Other direct payroll burden

Total loaded labor cost

Then compare that loaded cost to the bill rate.

The formula becomes:

Bill rate minus loaded labor cost = true gross profit

And:

True gross profit divided by bill rate = true gross margin

This gives owners a much clearer picture of whether a placement is actually supporting the business.

Why Burden Rates Should Be Modeled by Role or Client

Not every client creates the same cost structure.

Some clients have:

Higher-risk job categories

More turnover

More workers’ comp exposure

More payroll complexity

Higher benefits participation

More admin follow-up

More timecard issues

If those differences are not reflected in pricing, the firm may undercharge for difficult or risky work.

The better approach is to model burden at least by:

Role type

Workers’ comp class

Client

Department or location

Placement type

W2 vs contractor structure

This does not need to be overly complicated.

But it does need to be more detailed than one blended percentage across the entire firm.

How Incorrect Burden Modeling Hurts Margin

Burden rate issues usually do not show up all at once.

They show up slowly.

A few common problems include:

1. Pricing Too Low for High-Burden Roles

If workers’ comp and payroll burden are underestimated, the firm may accept bill rates that do not leave enough margin.

The placement may look fine in the sales conversation but underperform once payroll and insurance costs are included.

2. Thinking a Client Is Profitable When It Is Not

A client with steady volume can look attractive.

But if that client has high-risk roles, frequent turnover, or heavy payroll burden, the true margin may be weak.

Revenue can hide the problem.

Cash flow usually exposes it later.

3. Comparing Recruiters or Clients Incorrectly

If burden is not modeled properly, performance reporting becomes misleading.

One recruiter may appear to generate better margin simply because they work on lower-burden roles.

Another may look weaker because they serve clients with higher delivery costs.

Without loaded labor cost, comparisons are incomplete.

4. Letting Blended Gross Margin Hide Risk

Overall gross margin can look acceptable while specific placements are barely profitable.

This is especially dangerous when high-volume clients carry low true margin.

The firm gets busier, payroll grows, and cash pressure increases, but profit does not improve enough.

Warning Signs Your Burden Rate Model Is Too Simple

Burden rate problems usually show up indirectly first.

Common warning signs include:

Gross margin looks fine, but cash still feels tight

Certain clients create more stress than their revenue justifies

High-volume accounts do not seem to improve profit

Workers’ comp renewals create surprises

Pricing decisions are based mostly on competitor rates

You are not sure which placements are truly profitable

Payroll grows faster than cash reserves

If any of these feel familiar, the problem may not be sales volume.

It may be delivery cost visibility.

What to Review Before Changing Prices

The instinct is often to raise rates across the board.

That may be necessary, but it should come after you understand the numbers.

Before changing pricing, staffing firm owners should review:

Burden rate by workers’ comp class

Loaded labor cost by role

Gross margin by client

Gross margin by placement type

Payroll tax and benefit assumptions

Historical workers’ comp cost trends

Client-level admin burden

This helps prevent overcorrecting.

Some clients may need a pricing change. Others may be fine. Some roles may be profitable only at a higher markup. Others may already support the business well.

The goal is not to raise prices blindly.

The goal is to price based on actual delivery cost.

Final Thought

In staffing, the pay rate is only the beginning of the cost story.

Workers’ comp, payroll taxes, benefits, and other burden costs determine whether a placement actually creates profit or just creates activity.

A healthy staffing firm does not just know its bill rates and pay rates.

It knows its true loaded labor cost.

If your margins look acceptable but the business still feels tighter than it should, your burden rate model deserves a closer look.

In our Accounting Review, we help staffing firm owners break down true delivery cost by client, role, and burden category so they can see which placements are actually creating profit and which ones are quietly eroding it.